TCFHC upholds a customer-centric service philosophy and strictly complies with relevant regulations to ensure transparency and fairness in all business activities. To enhance service quality and customer experience, TCFHC continues to provide comprehensive communication and complaint-filing channels, ensuring that customer rights and interests are protected while creating maximum value and trust.

Customer Relationship Management

To improve customer service quality, TCFHC engages with consumers every year to listen carefully and understand their opinions on financial products and services. For customer complaints, the Group has established a comprehensive classification system and handling procedures to ensure that customer issues are resolved effectively within the required timeframe and that customer rights and interests are safeguarded.

Customer Satisfaction

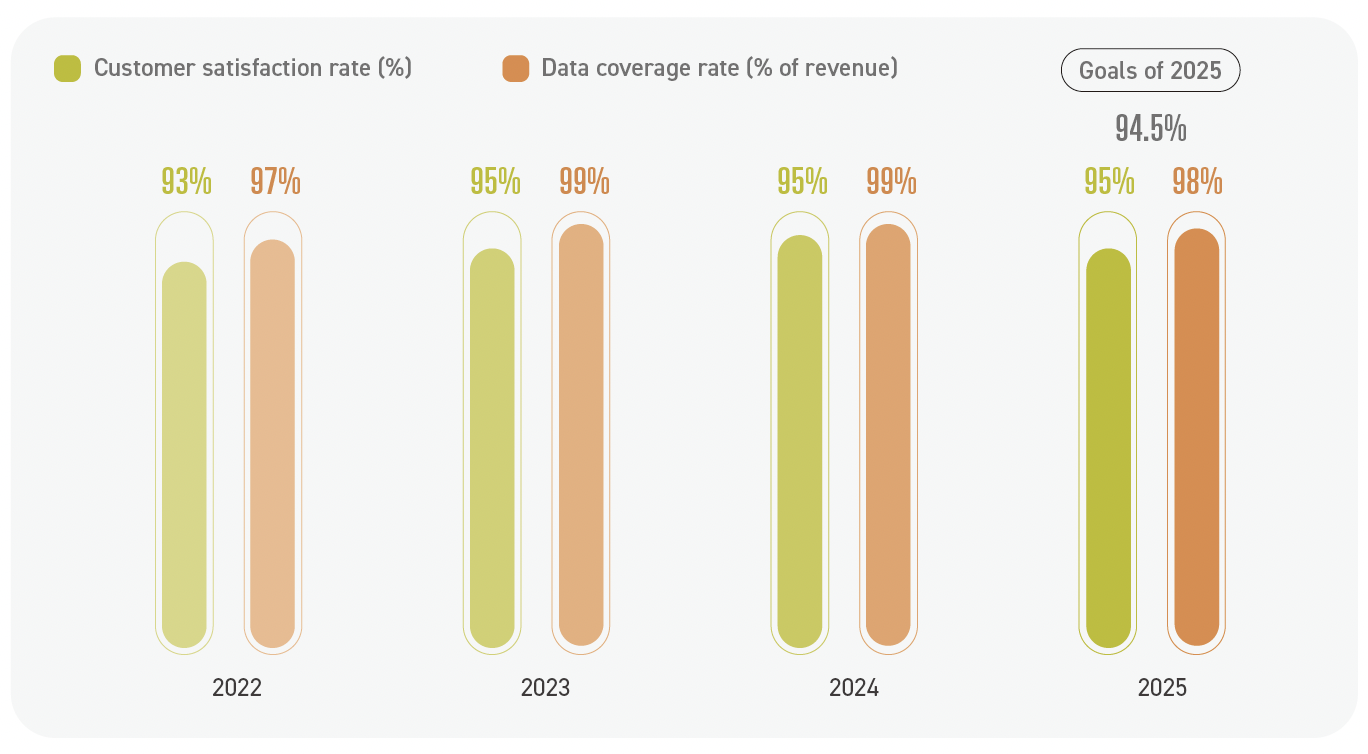

TCB, TCS, and BNP TCB Life conduct customer surveys every year and periodically track and review the achievement of customer satisfaction goals, with the aim of providing comprehensive and sound protection of customer rights. In particular, TCB also conducts a mystery shopper program with external service providers, under which professionally trained reviewers act as customers to evaluate areas such as counter service, environmental cleanness, and phone courtesy. After the evaluation is completed, training sessions are conducted to help each business unit fully understand areas for improvement and make the necessary enhancements. BNP TCB Life and TCS, on the other hand, conduct customer satisfaction surveys by telephone through randoml sampling. Based on the survey results, they comprehensively review areas in the service process requiring improvement to continuously optimize the overall service experience.

Customer Communication Channels

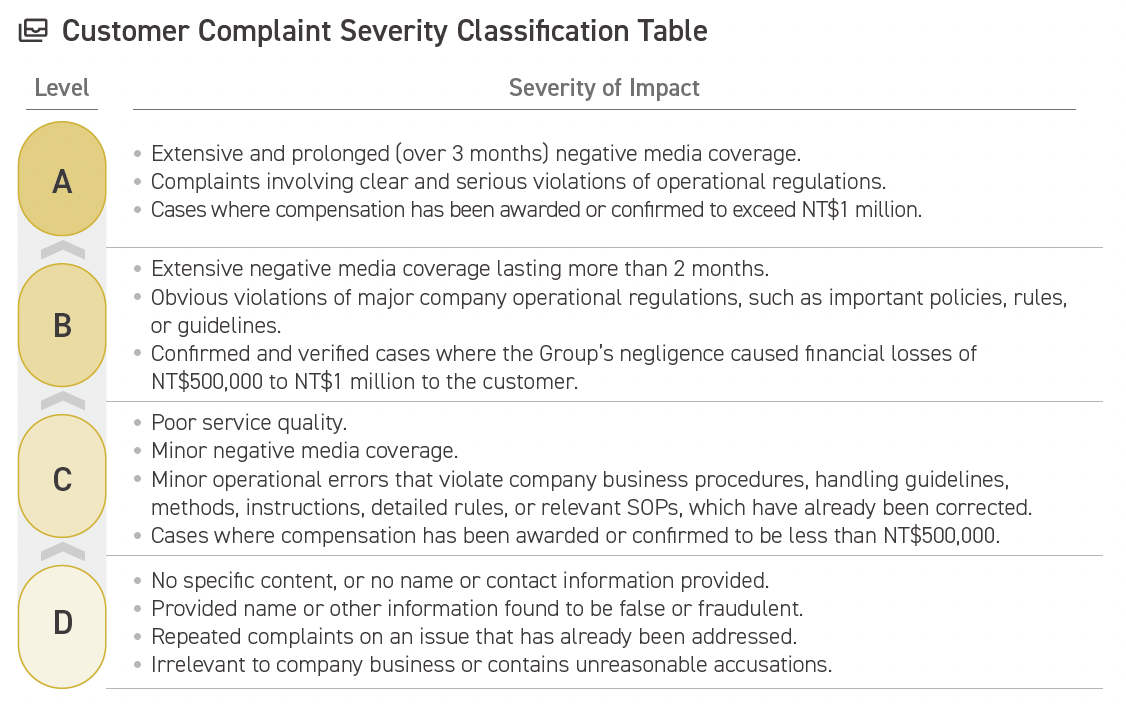

TCFHC has set up smooth communication and complaint channels, including a hotline and email. Once the Group receives a customer complaint, the case is registered and handled in accordance with its customer complaint procedures. Throughout the handling process, the Group complies with the "Personal Information Protection Act" to protect customers' privacy. The handling process and related improvement measures are then reported to the president to ensure further enhance customer service. In 2025, the Group received a total of 390 customer complaints. Among them, 21 were classified as Grade D and the remainder as Grade C; all have been properly handled and closed.

TCB introduced the BSI "ISO 10002:2018 Quality management - Customer satisfaction - Guidelines for complaints handling in organizations" in 2023 to optimize its internal procedure by referring to the international complaints handling mechanism. Besides comprehensive review of complaints filed, the responsible unit is asked to get to the bottom of the complaint and precisely enforce the corrective action to ensure that the issues are corrected. Meanwhile, the complaint handling status is available for inquiry on the official website through the message box for guaranteed information transparency and to protect customer rights.

In terms of handling timeliness and follow-up, TCB adopts a proactive approach. Customers are notified immediately after a complaint is successfully submitted. In principle, customers receive an initial responses within 5 business days of filing a complaint, and complaints are expeceted to be properly resolved and closed within 30 days. For complex cases where a timely response is not possible, an extension is requested in accordance with the relevant procedures. In addition, to ensure that customer appeals are properly addressed and responded to, customer feedback is followed up within 30 days after a case is closed, demonstrating through concrete actions TCB's commitment to protecting financial consumers.

Combating Financial Fraud

In response to increasingly sophisticated fraud schemes, TCB has formed the cross-departmental anti-fraud taskforce that brings together business units, compliance personnel, and technology teams. Through a three-pronged approach of "ex-ante prevention", "in-process review", and "ex-post monitoring", TCB proactively manages high-risk accounts as part of a comprehensive internal anti-fraud control mechanism. In accordance with the "Regulations Governing the Deposit Accounts and Suspicious or Unusual Transactions" and "On-site Customer Care Questioning", TCB enhance KYC procedures, customer care questioning, and controls over dummy accounts when customers make deposits, withdrawals, or remittances at the counter. Common suspicious or apparently abnormal transaction patterns are incorporated into the daily report and the AI early-warning model. On a daily basis, TCB's business units verify the legitimacy of customer transactions based on trigger patterns and and early-warning lists. Where suspicious or abnormal activities are identified, electronic translations may be suspended as a control measure. Through continuously daily monitoring, TCB seeks to intercept illicit fraudulent cash flows in a timely manner. TCB also maintains a comprehensive abnormal cash flow reporting system. Its 24-hour customer service center handles joint defense alerts and reports, and TCB has established the "Early Warning Mechanism for Bank Accounts Suspected of Domestic/Overseas fraud". Through close cooperation between the financial sector and the police, these measures help prevent customers from falling victim to fraud. To strengthen technology-enabled fraud prevention, TCB introduced an AI anti-fraud early-warning model in 2024 and integrated it into the "FraudSeer" platform in 2025. By combining the AI model with maual review, the platform enhances suspicious transaction alerts. Model parameters are adjusted on a rolling basis according to customer characteristics and transactional patterns, enabling risk-based monitoring and control high-risk accounts. To ensure the effective implementation of anti-fraud measures, TCB completed mystery shopper checks at 65 business units in 2025, randomly reviewing the verification and control procedures applied to model-generated warning lists. TCB also actively participates in the FISC "Financial Anti-Fraud Joint Defense Platform". Through functions such as "real-time verification", "early cash-flow inquiry", and "joint-defense broadcast", the platform establishes an information-sharing mechanism to help identify suspicious transactions. TCB has also established a list of potential victims and linked it to data from the Criminal Investigation Bureau and the potential victim data provided through the "joint defense broadcast" of the Financial Anti-Fraud Joint Defense Platform. When customers conduct counter withdrawals or remittances, reminder messages are generated, and the police may be notified as needed.

In terms of law enforcement collaboration, the Company has signed the Memorandum of Understanding (MOU) on Anti-Fraud Cooperation with the Criminal Investigation Bureau. It also works with the Taiwan High Prosecutors Office to support District Prosecutors Offices throughout the nation in promoting the "Suspicious Account Monitoring Mechanism". The Company has signed the Memorandum of Understanding (MOU) on the Suspicious Transaction Analysis Mechanism Project, and has jointly signed an MOU on the Suspicious Transaction Analysis Mechanism Project with the Office. In addition, the Company has established an ATM "Grey List" Transaction Reporting and Early-Warning Mechanism. To protect transaction security, TCB has comprehensively adopted the dedicated SMS code for financial industry when sending marketing, transaction verification and other transactional text messages.It also offers the real-time account holder inquiry mechanism for ATM, online banking, and mobile banking transfers and deposits, and offer real time monitoring and notifications for credit card, online banking, and mobile banking log-ins, helping customers identify official messages and block fraudulent ones. At the same time, TCB regularly release anti-fraud announcements and posts, the latest anti-fraud videos or cases and anti-fraud online games on its official Facebook page, LINE bulletin board, official website, branch lobbies, and ATMs, working together with the public to build a comprehensive financial protection network.

TCB actively promotes anti-fraud awareness. In 2025, anti-fraud courses were included in TCB's digital learning programs and in 83 in-person employee training sessions, with total attendance reaching 14,402. To enhance public awareness of fraud prevention and fraud identification, TCB also organized 591 anti-fraud awareness activities in schools and communities, as well as joint outreach events with the police, attracting a total of 34,457 participants. In addition, at the 2025 Taipei International Financial Expo, TCB featured financial fraud prevention as one of its exhibition themes. During the three-day event, approximately 2,300 visitors completed the anti-fraud interactive experience, and 300 participants attended the financial literacy and anti-fraud awareness seminar, helping convey the importance of financial fraud prevention to the public.

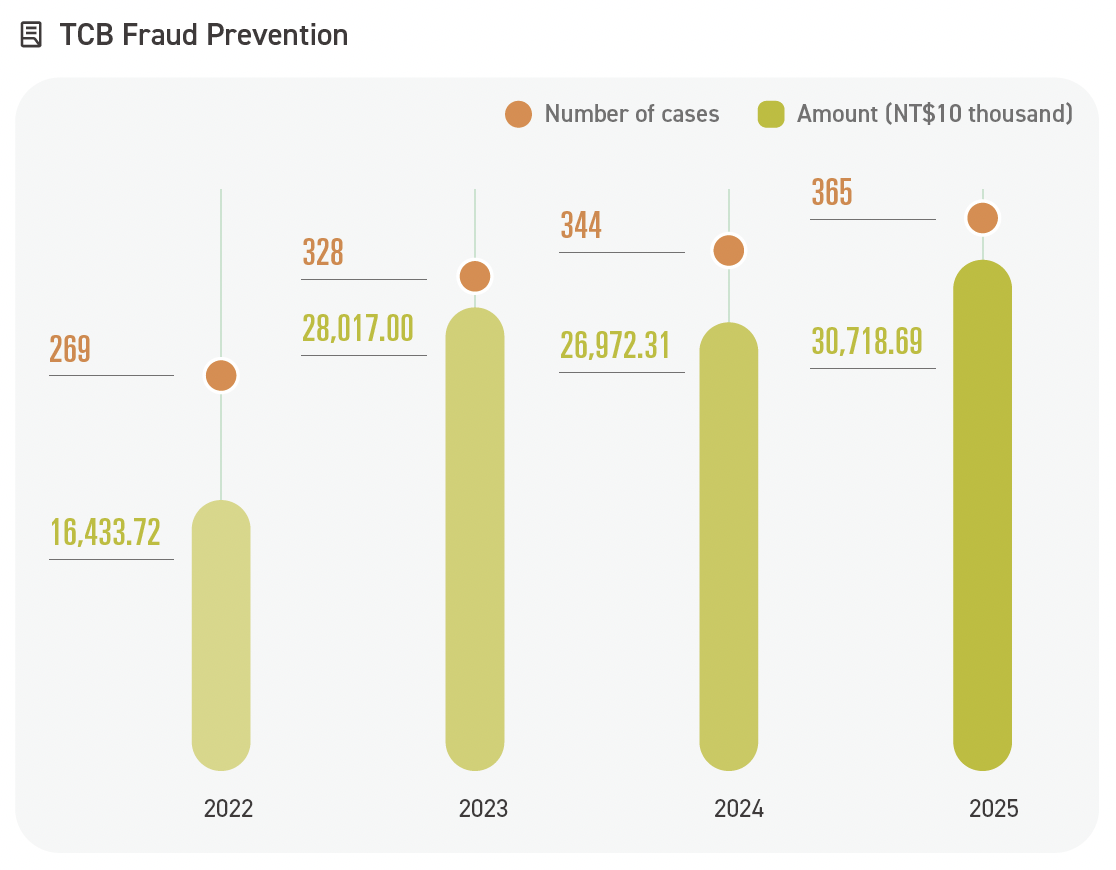

To encourage employees to help prevent the public from falling victim to fraud, TCB has established an incentive mechanism for employees who intervene in fraud attempts. Depending on the amount prevented, employees are awarded either bonuses or commendations. In 2025, a total of 365 cases were stopped, preventing approximately NT$307 million in losses. A total of 77 commendations were granted, and NT$682,000 in bonuses was awarded. Besides individaul incentives, TCB has newly added compliance evaluation scores for business units that successfully prenvent fraud and recognizes outstanding anti-fraud employees at Board of Directors meetings, promoting fraud prevention as a culture of honor.

Fair Customer Treatment

TCFHC integrates the spirit of fair customer treatment into its service processes and corporate culture, while continuously strengthening employees' training to comprehensively protect the rights and interests of every customer.

Principles for Treating Customers Fairly

TCB established the "Consumer Protection and Fair Customer Treatment Promotion Committee" in 2019, with the president serving as the convener. The committee consists of an executive vice president, a chief compliance officer, and 22 heads of responsible business units as members. It is responsible for formulating policies and strategies related to the Principles of Treating Customers Fairly, handling significant consumer disputes, reviewing the progress and evaluation results of fair customer treatment, and periodically compiling customer complaints and cases handled by Financial Ombudsman Institution (FOI), together with the review and improvements status of various cases, for submission to the Board of Directors.

TCB, TCS, BNP TCB Life, and TCBF have all established policies and implementation regulations related to the Principles for Treating Customers Fairly, and have also introduced regulations on friendly financial service. A dedicated unit centrally coordinates implementation, compiles execution results, and reports them to the Board of Directors. These measures ensure that employees uphold the principles of integrity and good faith in various aspects such as the sale of products and services, advertising and solicitation, complaint protection, and the professionalism of business personnel, while complying with the "Ethical Corporate Management Best Practice Principles", "Financial Consumer Protection Act", and "Financial Service Industry Principles for Treating Customers Fairly". Wealth management personnel are also required to sign the "Code of Conduct for Wealth Management Employees" before assuming their duties or conducting business, in order to protect customer rights and interests and enhance customer satisfaction. In addition, annual credit audits are conducted on wealth management personnel.

To implement friendly financial services, TCB has incorporated the principle of friendly service into its "Principles for Treating Customers Fairly" and established "Financial Friendly Service Guidelines" for all employees to follow. These guidelines stipulate that the needs of the elderly and people with disabilities must be proactively considered the needs of at every stage of financial products and services, from design to sales, and that fair treatment strategies should be implemented according to the characteristics of each business. In addition, to implement the monitoring mechanism for assessing the appropriateness of financial services, TCB actively and properly addresses customer messages from the elderly and people with disabilities, while optimizing its internal message-processing system and external message mailboxes.

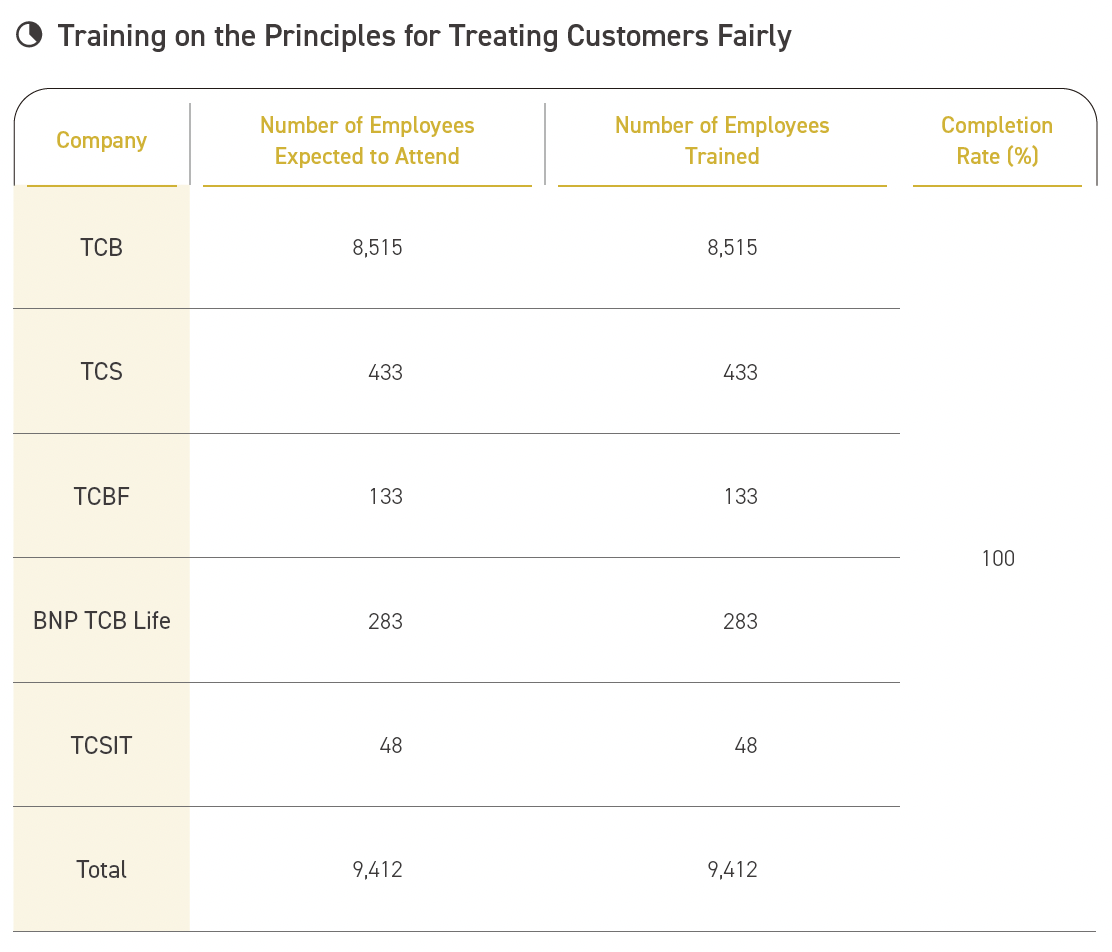

To strengthen a top-down culture of treating customers fairly, TCB held the seminar "Advanced Workshop on the Principles of Treating Customers Fairly" in August 2025. Members of the Financial Ombudsman Institution were invited to share practical topics such as "Insights of Reviewed Cases", "Financial Friendly Services" and "Convention on the Rights of Persons with Disabilities (CRPD)" with senior management personnel, including directors, deputy general managers, the chief compliance officers, the chief auditors and head of units, in order to improve their professional skills. At the same time, TCB is committed to extending the concept of friendly financial services to frontline staff. In 2025, the bank held a total of 28 financial friendliness-related courses, with 9,090 employees attending. The group's subsidiaries also regularly conduct employee training, internal assessments, and mystery shopper reviews to monitor the implementation status of the Principles for Treating Customers Fairly and to formulate corrective measures accordingly, ensuring that fair customer treatment and friendly financial services are embedded in in every customer interaction.

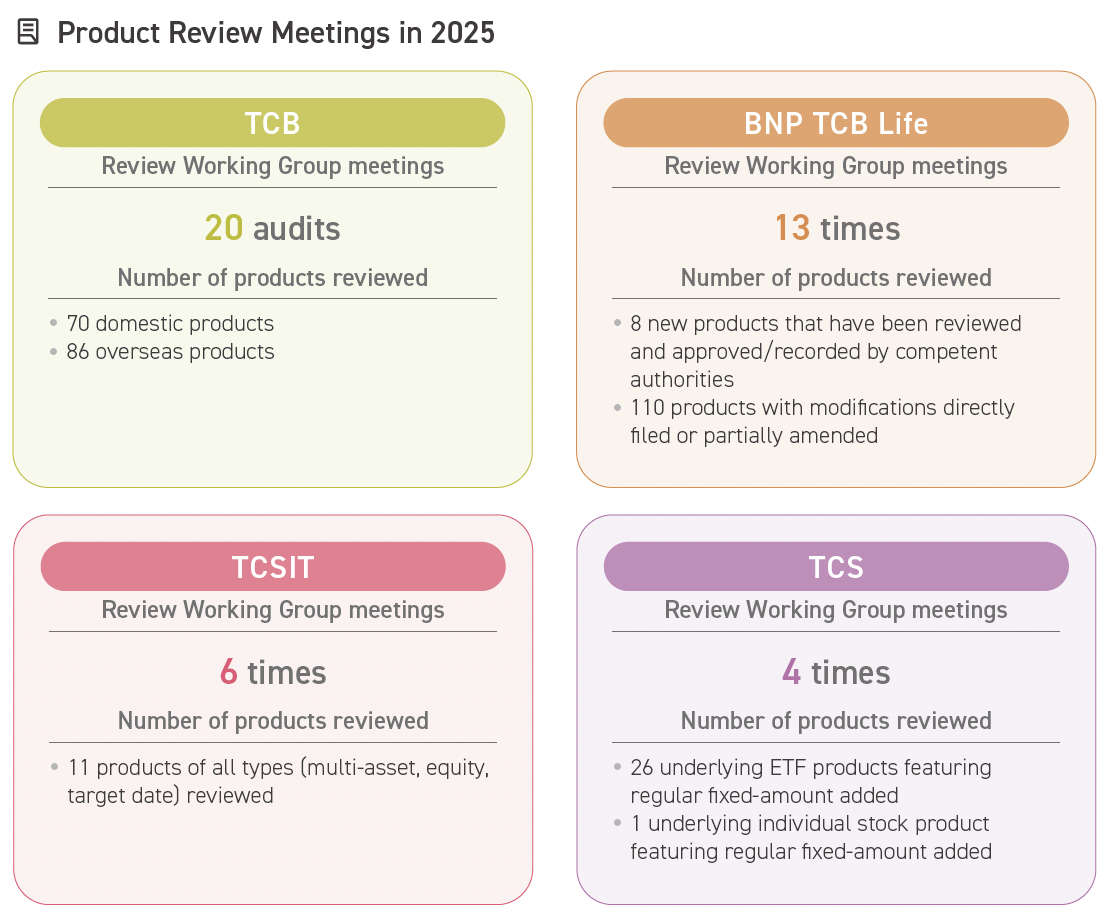

Procedures for Product Review

All of the financial products or services launahced by the Group take customer needs into consideration throughout the processes of design and planning, promotion, marketing, contract performance, service consultation, complaint handling, and financial consumer dispute resolution, so as to ensure that customers are treated fairly and reasonably. In addition to complying with the Financial Consumer Protection Act and the regulatory requirements applicable to each line of business, internal reviews are also required to ensure that products do not contain improper content, untruthful statements, or other elements that may mislead consumers or violate laws and self-regulatory rules. If a products requires approval from the competent authorities before launch, its appropriateness must still be reviewed in a timely manner based on actual sales conditions, consumer feedback, and applicable laws. Before the Group enters into a contract with a customer to provide financial products or services, it shall adhere to the principles of fairness, reasonableness, equality, reciprocity, and good faith, fully explain the material terms of the financial products, services and contracts, and disclose risks.

Privacy Protection Policies and Management

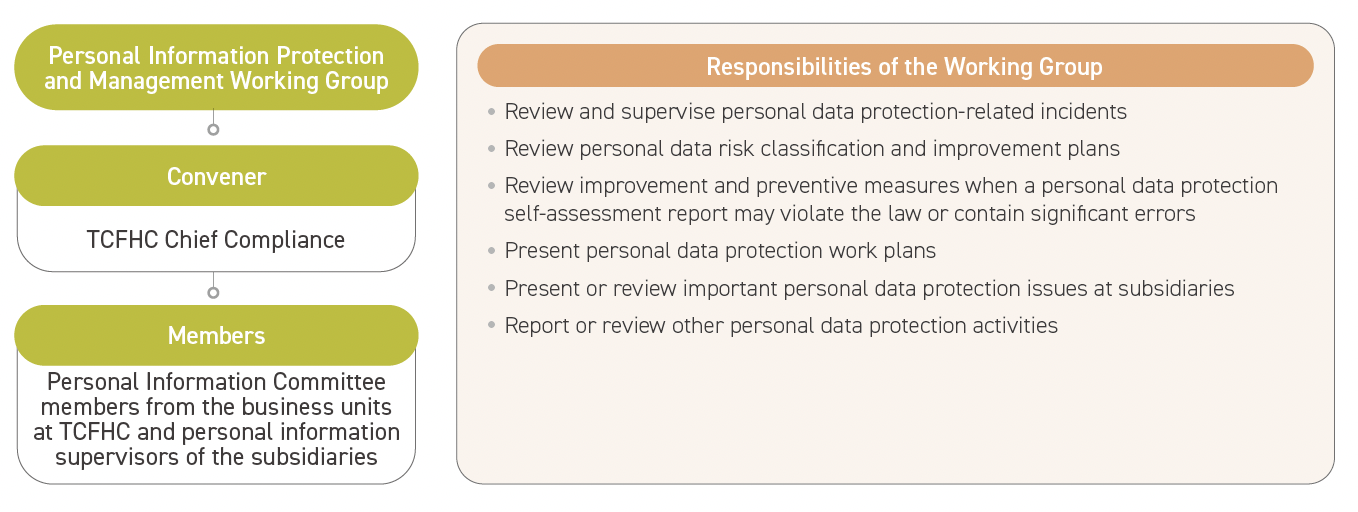

As the financial businesses operated by each subsidiary involve a large amount of personal information, the Group follows and implements privacy protection through three aspects: "Customer Information Confidentiality", "Privacy Statement on the Sharing of Customer Information", and "Protection of Personal Information". Related management measures have been incorporated into the responsible unit's "Checklist of Self-Evaluation on Legal Compliance", which is conducted every six months.

Customer Information Confidentiality

The Company has defined the "Customer Information Confidentiality Measures" and announced it on the official websites of the Company and each subsidiary so that respective subsidiaries throughout the Group fulfill their duty to keep customer information confidential while conducting joint marketing business. The content specifies the methods for collecting customer data, data storage, and safekeeping methods, information security and protection measures, data classification, scope and items of use, purposes of use, disclosure parties, methods for modifying customer data, handling of customer's refusal to receive messages related to the Group's joint marketing activities or to allow the Group cross-utilize their information, and disclosure of subsidiaries that cross-utilize customer data.

Privacy Statement on the Sharing of Customer Information

To improve customer convenience, strengthen the Company's risk management, and promote cross-industry cooperation among financial institutions while ensuring consumer rights, the Company has formulated the "Regulations for Sharing Data between Financial Institutions". Under the principle of information security, these regulations allow the appropriate use of customer data. The Company has established a control mechanism for data sharing among financial institutions within the Group. It has also disclosed the "Privacy Statement on the Sharing of Customer Information" on the official website, which includes customer protection measures in data sharing and methods for protecting customer rights and interests, thereby improving transparency in data sharing and enhancing customer trust.

Protection of Personal Information

The Company has formulated the "Personal Data Protection Management Policy" , which applies to the Company, its subsidiaries, and suppliers entrusted by the Company and its subsidiaries to collect, process, or use personal data, in order to implement the Group's protection of personal data and privacy rights. Meanwhile, the Company has also established the "Personal Data File Security Maintenance Measures" and the "Personal Data File Security Audit Mechanism". All subsidiaries have likewise established personal data protection management policies or usage guidelines. For example, TCB governs and fully discloses on its official website matters relating to the "nature of customer data", "method of use", "retention period", "access, transfer, amendment, and deletion", "disclosure to third parties", and "freedom to choose whether to provide relevant personal data and the types of data", so as to inform customers of their rights and interests. Full disclosures or notifications are also provided in products or services descriptions. In addition, mechanisms are in place for updating related information, cancelling data use, and filing complaints.

The Company and its subsidiaries have also established operational organization for personal data protection management to promote and handle the security audits of personal data files, develop acceptable risk thresholds for personal data files, and conduct risk assessment and self-assessment operations for personal data files. In addition, according to the "Personal Data Protection Management Policy", the Company is required to conduct internal audits on a regular basis to check the effectiveness of the personal data protection management system and its implementation. In accordance with regulatory requirements, subsidiaries are required to engage external institutions to conduct audits. For example, TCB and TCBF include personal data protection management in the annual internal control system audits conducted by certified public accountants, while BNP TCB Life engages accountants annually to perform compliance assessments. These measures help monitor and improve the effectiveness of personal data protection management. In 2025, TCB and BNP TCB Life obtained the "BS 10012:2017 Personal Information Management System" international standard certification and maintained the validity of their certificate.TCS also completed external verification under the Taiwan Personal Information Protection & Administration System (TPIPAS), successfully passed the renewal verification, and continued to maintain the validity of its TPIPAS verification.

Procedures for Handling Privacy Protection

In response to security incidents involving personal data being stolen, altered, damaged, destroyed, or disclosed, the Company has established the "Response Notifications and Preventions of Personal Information Breach". Each subsidiary has also implemented personal data incident handling and reporting procedures. For example, TCB follows the "Guidelines for Handling and Reporting Personal Information Security Incidents" when handling personal information incidents involving information leakage. For general personal information incidents, the responsible units should be notified, investigate the cause, notify the parties involved in an appropriate manner, and discuss corrective and preventive measures.Where customer information is involved and the incident is classified as material, a Crisis Management Taskforce will be formed to maintain close communication with the parties involved and issue a standard press release as needed. In addition, the Group has also established regulations such as the "Personal Data Protection Management Policy" and "Employee Reward and Punishment Points". Any employee found to have leaked business secrets or violated internal regulations will receive reprimands, demerits, or even termination of employment as punishment. In addition, if suppliers or their staff violate applicable regulations governing personal data protection or agreements concerning the protection of personal data, resulting in damages borne by the Company or its subsidiaries, they will be responsible for indemnification. In 2025, apart from the incorrect mailing of two insurance policies due to an operational error by the outsourced vendor of BNP TCB Life, which affected two customers (accounting for 100% of personal data–related information leakage incidents), the Group had no data breach incidents or affected customers in any of its other subsidiaries, nor were there any penalties for violating data protection equirements. In addition, in terms of TCB's use of customer personal data, approximately 48.94% of customer data was reused in compliance with relevant regulations or agreements with customers.

Training and Education on Privacy Protection

The Group regularly organizes personal information protection training. For example, TCB provided the "Awareness Promotion and Educational Training on Personal Data Protection Management", and BNP TCB Life rolled out "Personal Information Protection Courses" on its digital learning platform to raise security and legal awareness regarding the use of personal information in daily operations.