The compliance system is an important part of internal control and serves an anti-money laundering and combating the financing of terrorism purpose while deterring other illegal activities. It also prevents key compliance items that endanger the Company’s operations and cause disruption in the financial market. TCFHC implements relevant organizational frameworks, regulations, and rules to equip itself with abilities to address regulatory or environmental changes at any time and supervise its legal compliance status. TCFHC also provides internal training in order to avoid legal risks arising from violation of law and to fulfill a financial institution’s role by protecting customers’ rights.

Compliance Operations

TCFHC has established the "Rules for Implementation of Regulatory Compliance System" according to the "Implementation Rules of Internal Audit and Internal Control System of Financial Holding Companies and Banking Industries". The "Legal Compliance Committee" is also put in place to devise relevant organizational structures, rules and regulations in order to monitor regulatory compliance.

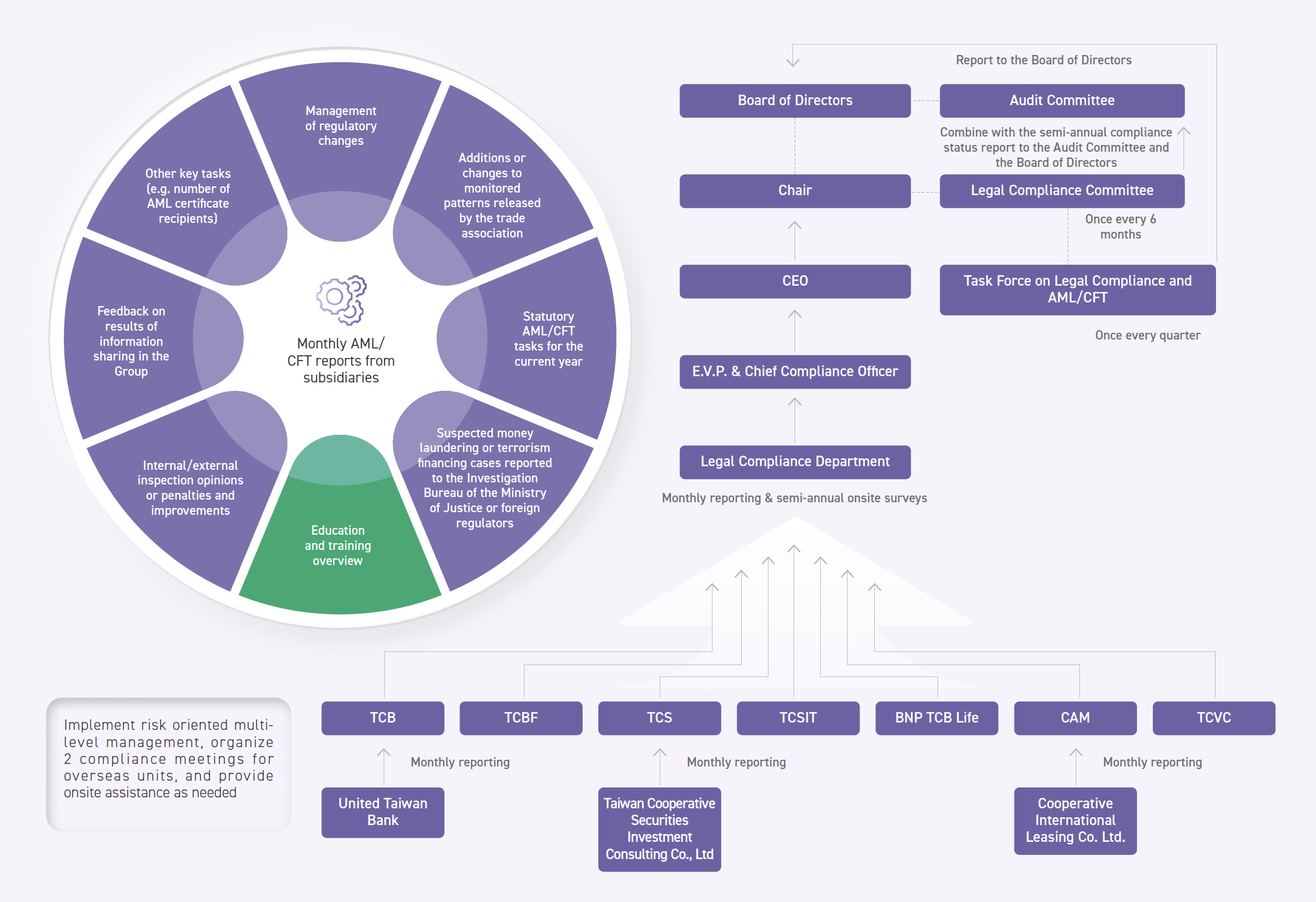

Regarding compliance audits by the FSC and regulators of affiliated business units, all penalties should be reported immediately to the relevant departments to ensure appropriate response and prevent repeat or further losses. TCFHC sets up "consistent and real time intercommunications" mechanism, which requires each subsidiary report to the TCFHC’s Legal Compliance Department the full account of inspections on legal compliance and AML/CFT during the entire course from inception of the inspection to completion of the draft if it happens to have financial competent authority to inspect.

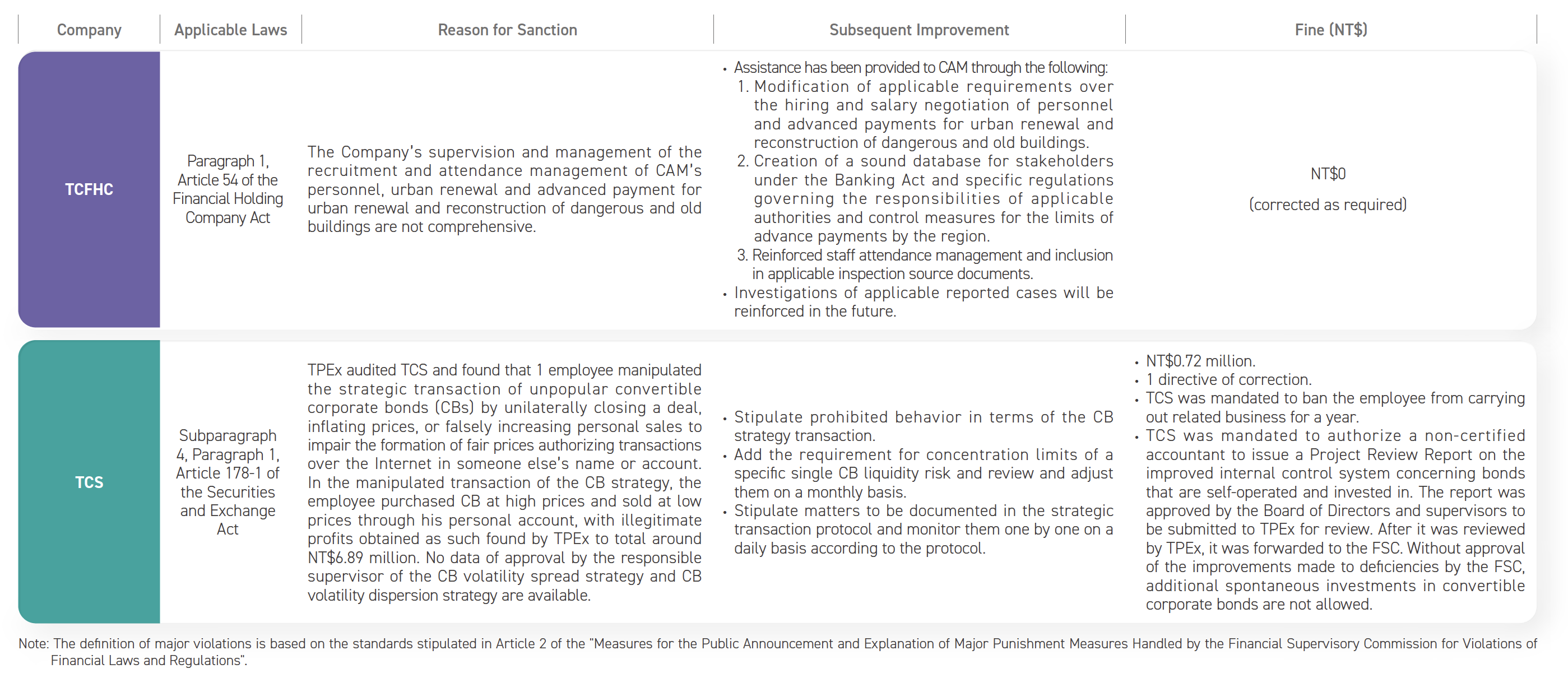

Punishment by Financial Competent Authority and Affiliated Business Units in 2023 and Corresponding Improvements

In 2023, the Group was not imposed significant penalties or disciplinary measures by competent authorities due to the violation of environmental or social law, or regulations. Yet the remaining penalties as received and related improvements are listed as follows:

Anti-Money Laundering and Combating the Financing of Terrorism

Policies and Systems

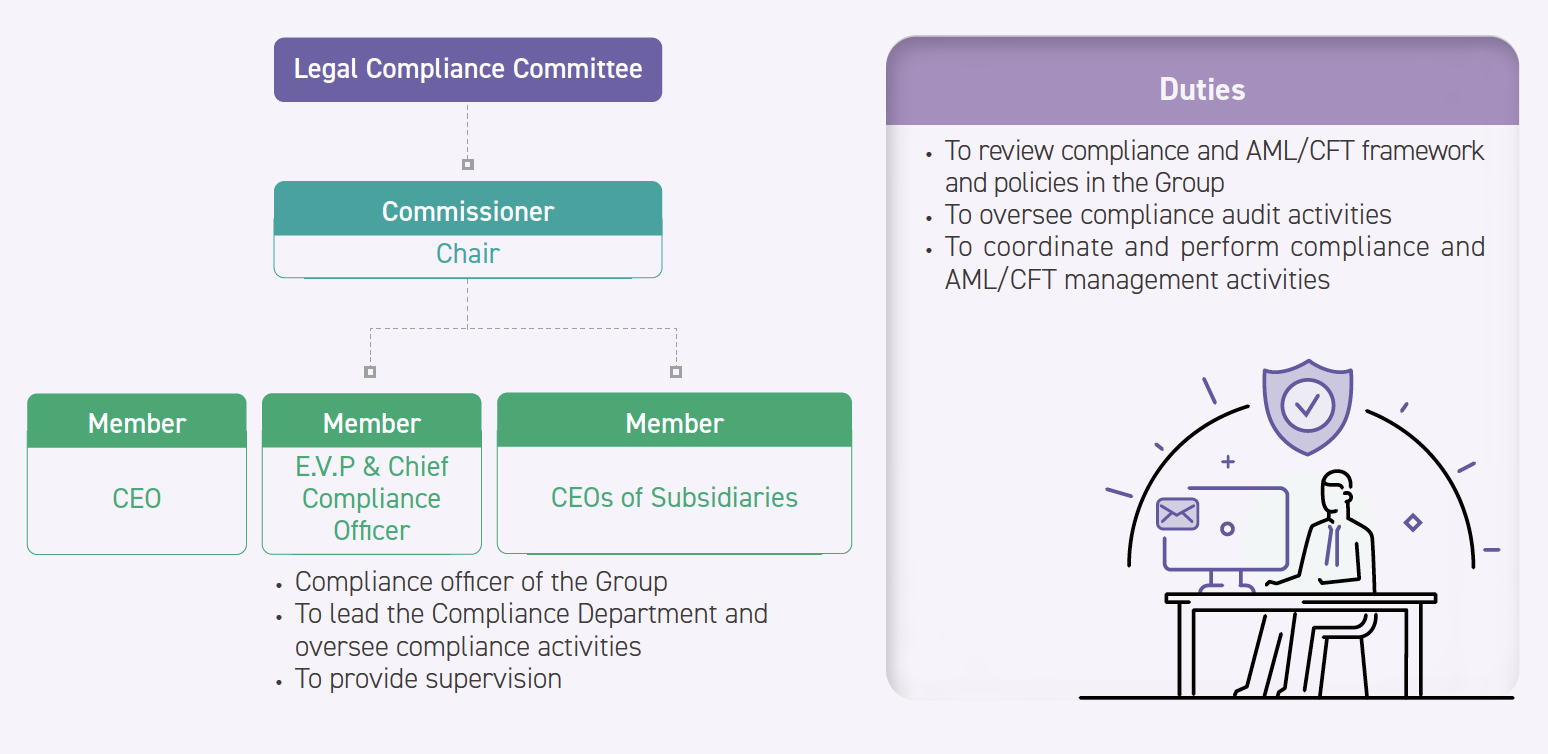

In order to properly implement anti-money laundering and combating the financing of terrorism, the Company has formulated "TCFHC and Subsidiaries General Anti-Money Laundering and Combating the Financing of Terrorism Plan." The content includes indicators of group level risk appetite, group’s framework for coherent risk assessment, and group’s procedures for information sharing. The plan clearly specifies identification, evaluation, and management principles of money laundering and terrorism financing risks to comply with. Each subsidiary has also established relevant policies and procedures for the framework of money laundering and terrorism financing risks assessment. They also regularly conduct comprehensive assessment of such risks and report to the Board of Directors. Risk assessment reports are also submitted to FSC for reference. The Legal Compliance and AML and CFT Task Force was established at the same time, where the E.V.P. & Chief Compliance Officer serves as the convener to take charge of supervising and coordinating the implementation of legal compliance and AML and CFT tasks of respective subsidiaries and submitting the operational status of the task force on a quarterly basis to the Company’s Board of Directors.

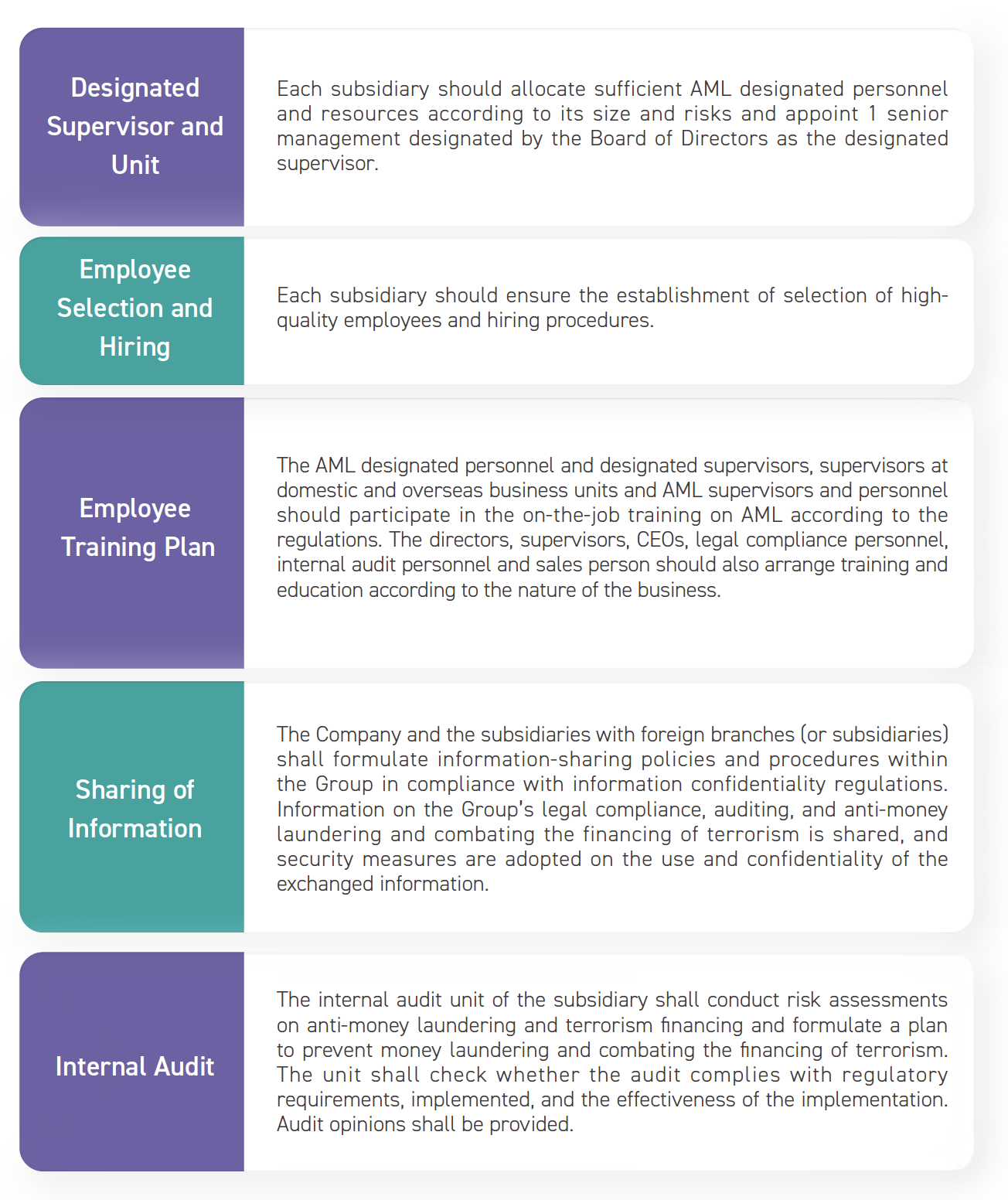

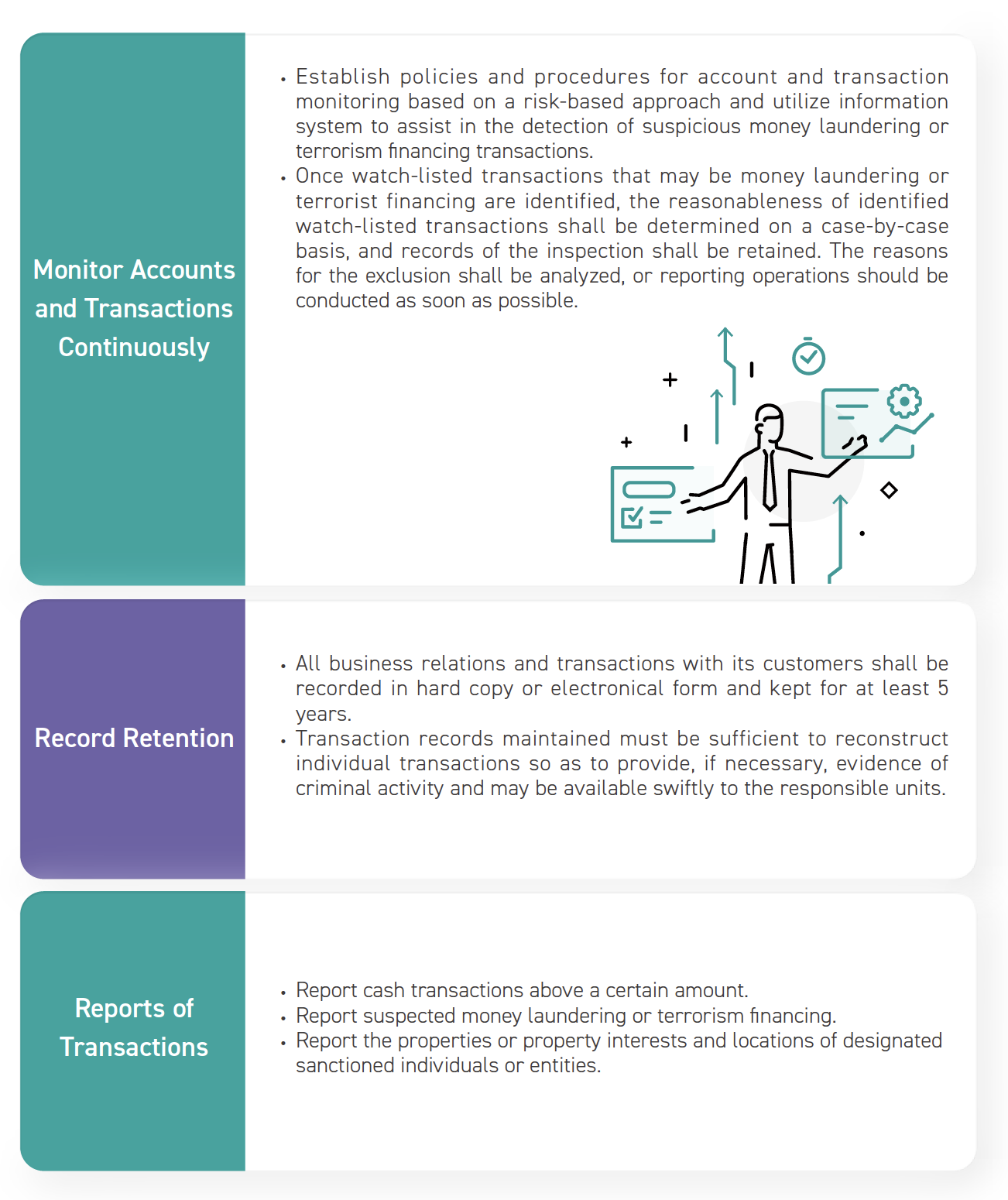

Each subsidiary also works to optimize each of their information system on anti-money laundering and combat of terrorism financing, with which databases are linked and carefully analyzed and monitored to ensure effectiveness of risk control and management on money laundering and terrorism financing. The content of anti-money laundering and combating the financing of terrorism regulations for each subsidiary includes but is not limited to the following:

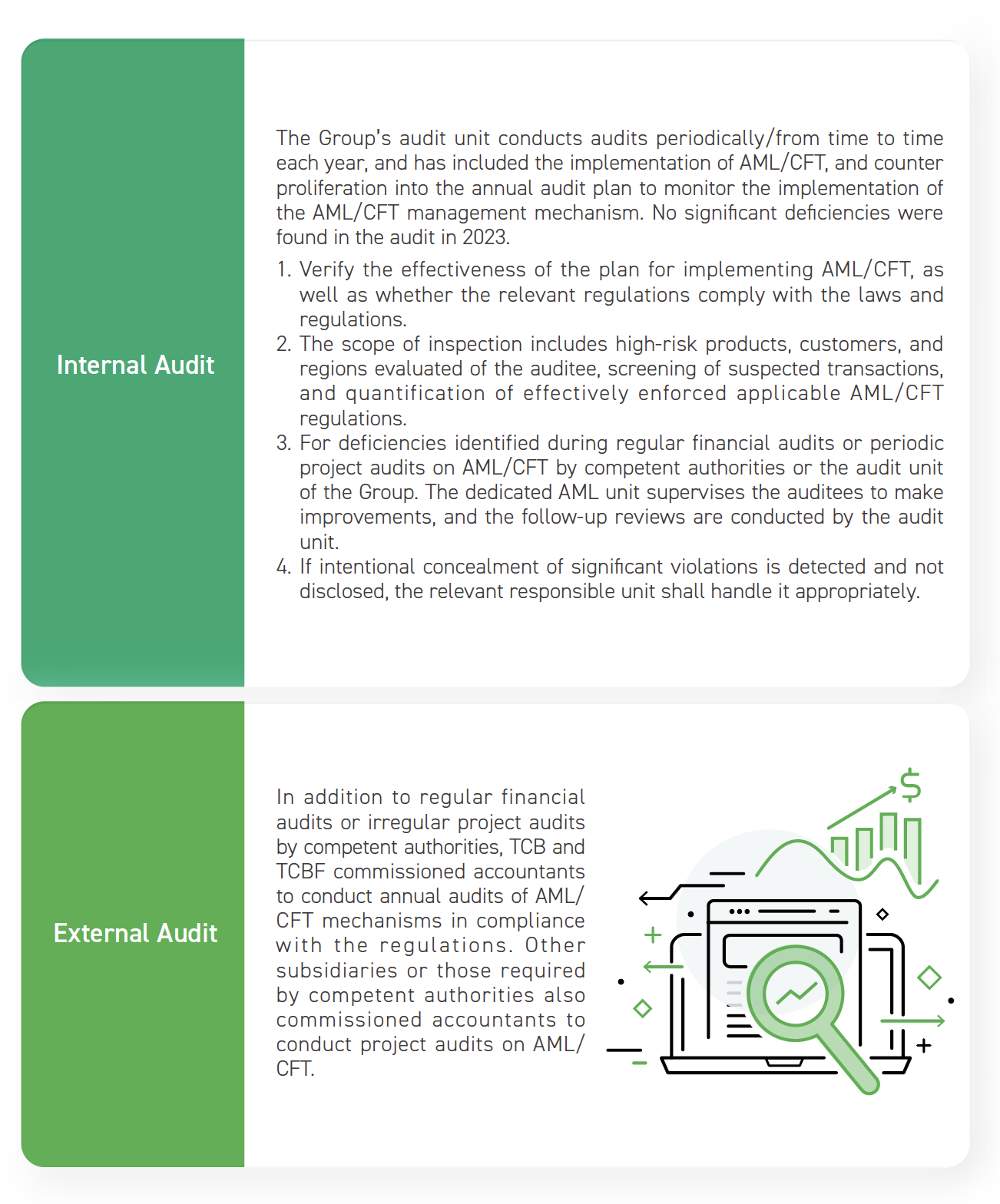

Independent Audit Mechanism for the Year

Strengthen AML/CFT Capabilities

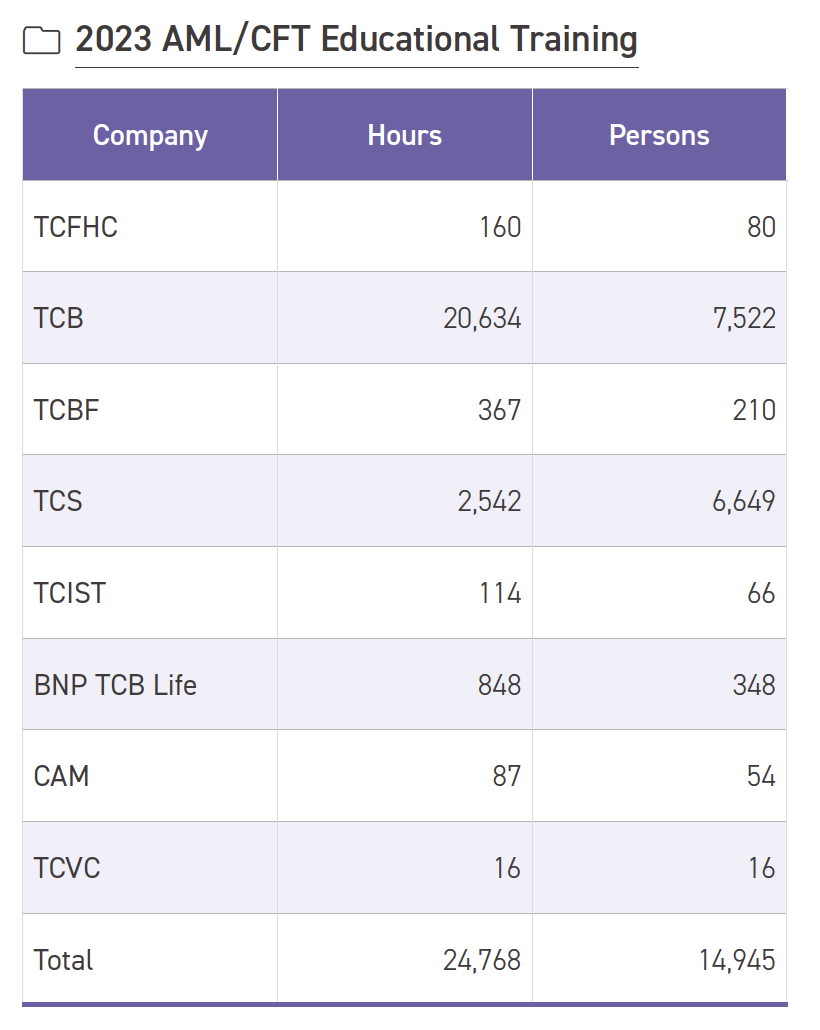

In order to further increase awareness of regulatory framework on anti-money laundering and combating the financing of terrorism among employees, relevant educational trainings that the Group had organized in 2023, had received a total of 14,945 participants with a total training length of 24,768 hours. Additional education trainings on anti-money laundering and combating the financing of terrorism for directors, supervisors, senior management, and employees are also held every year with the expectation to raise awareness of legal compliance and professional capability. The Group also encourages employees to obtain the Certified Anti-Money Laundering Specialist (CAMS) and domestic certification for AML/CFT professionals. As of the end of 2023, 6,680 people, or 75.28%, in the Group had obtained such credentials.